Here is a number that should embarrass the global banking system: 8.78%.

World Bank

That is the average cost of sending $200 to Sub-Saharan Africa as of Q1 2025, according to the World Bank’s Remittance Prices Worldwide report. The global average for the same transaction is 6.49%. The G20 target — a target set in 2014 and still unmet — is 3%.

Africa is not behind by a little. Africa is behind by a factor of nearly three.

And the cost is only part of the problem. The other part is time. Traditional cross-border payments across the continent take between three and seven business days to settle — days during which your working capital sits locked in transit, your counterparties wait, and your business stands still. On some corridors it is worse. The South Africa to Zimbabwe corridor has recorded costs as high as 12.7%. South Africa to Malawi has historically hit 24%.

These are not edge cases. These are the normal conditions under which African banks, fintechs, corporates, and financial institutions operate every single day.

The question is not whether this is broken. The question is why — and what actually fixes it.

The Correspondent Banking Chain Is Not Built for Africa

To understand why African cross-border payments are slow and expensive, you have to understand the infrastructure they run on.

Most international FX transactions do not travel directly from one institution to another. They move through a chain of correspondent banks — intermediaries with pre-existing relationships and accounts — that pass the transaction from link to link until it reaches its destination. Every link in that chain adds time. Every link adds cost. And every link introduces another point of failure.

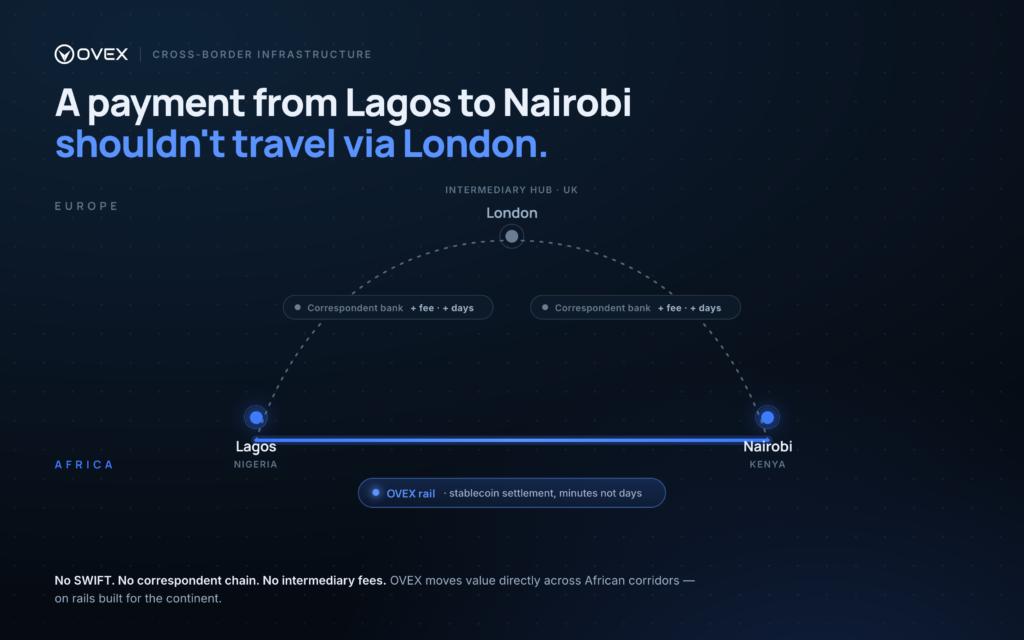

For major global corridors — US to UK, Germany to France — the chain is short, the volumes are high, and the costs are competitive. For African corridors, the chain is long, the volumes are comparatively thin, and the correspondent banks at each node are often located outside the continent entirely. A payment from Lagos to Nairobi may travel via London. A payment from Accra to Dakar may route through Paris. The continent’s financial infrastructure does not yet connect Africa to itself in a straight line.

This was tolerable when global banks had a strategic appetite for African markets. That appetite is now gone.

Between 2020 and 2026, tier-one global banks have systematically withdrawn from correspondent banking relationships across Africa — a process the industry calls de-risking. Barclays completed its century-long exit from Africa in 2022. Standard Chartered divested subsidiaries across Angola, Cameroon, Gambia, Sierra Leone, and Zimbabwe between 2022 and 2025. Société Générale sold off its Moroccan and Algerian interests. BNP Paribas shut down its South African investment banking arm in 2024.

Their stated reason: compliance cost and risk-adjusted return. Their actual message to African institutions: you are not worth the overhead.

The result is a liquidity gap. African institutions that once relied on global banks for FX execution are now navigating a correspondent banking landscape that is simultaneously more expensive, less reliable, and more thinly covered than it was a decade ago. The banks that built the infrastructure are leaving. The infrastructure itself has not been replaced.

Meanwhile, intra-African trade reached $192 billion in 2023, according to the Afreximbank African Trade Report 2024 — and is growing. The African Continental Free Trade Area is designed to push that number significantly higher. The financial rails to support it are not keeping pace.

What the Market Is Actually Telling You

When formal systems fail, markets find workarounds. The data on this is unambiguous.

Stablecoin usage across Africa and the Middle East represented an estimated 6.7% of total regional GDP as of 2024 — one of the highest adoption rates anywhere in the world, according to a 2025 IMF Working Paper. That is not a technology trend. That is a verdict on the banking system.

African businesses and individuals are not turning to digital dollars because they are early adopters. They are turning to them because the alternative — a correspondent banking chain that charges 8–12% and takes a week — is genuinely worse. When USDT settles in minutes and your bank settles in days, the choice is not complicated.

The market is not waiting for the infrastructure to be fixed. It is routing around it. The question for African financial institutions is whether to lead that shift — or be disintermediated by it.

The Direct Route to African Liquidity

OVEX Wholesale FX was built on a different premise: that if you want to move money across Africa efficiently, you have to build infrastructure specifically for Africa — not adapt a global template.

Over seven years, OVEX has built proprietary local-currency rails across 25+ African jurisdictions, established direct banking relationships in each market, and developed on-the-ground compliance expertise across a continent with 54 different regulatory environments. The result is FX infrastructure that is structurally different from the correspondent banking model — not faster correspondent banking, but a different kind of connectivity entirely.

T+0 settlement across supported corridors. Where the correspondent banking chain takes three to seven days, OVEX settles the same day. This is not a feature. It is a structural outcome of building direct rails rather than routing through intermediaries. For treasury desks managing FX exposure, for fintechs pricing cross-border products, for corporates with payroll obligations across multiple currencies — same-day settlement changes the economics of the business.

Tighter spreads. Deep liquidity pools, direct banking relationships, and institutional volumes allow OVEX to offer pricing that global banks — adding a margin on top of a margin — structurally cannot match. Custom wholesale rates scale with volume, frequency, and corridor, meaning the relationship becomes more valuable as it grows.

Local currency credit lines. This is perhaps the rarest offering on the continent. OVEX extends institutional credit lines denominated in African local currencies — ZAR, NGN, KES, and others — allowing clients to trade on credit and settle post-trade. Most FX providers require pre-funded accounts, locking up capital that businesses need for operations. OVEX does not. For treasury teams managing working capital across multiple corridors, this is not a convenience — it is a capital efficiency unlock that compounds over time.

Pan-African coverage with local expertise. 25+ jurisdictions. Offices in Cape Town, London, Paris, Nairobi, and Dakar. Local banking rails and compliance infrastructure in each market. OVEX is not a global bank visiting Africa. It was built here, by people who understand that what works in London does not automatically translate to Lagos or Lusaka.

Institutional-grade service. Every client receives a dedicated Relationship Manager with 24/7 WhatsApp support. Trades can be executed directly via WhatsApp — no platform login, no friction, no waiting until London’s business hours open. This mirrors the high-touch service model that global prime brokers offer their top-tier clients. OVEX delivers it with continental market knowledge.

Regulated across three continents. FCA (UK) for international remittance, FX, and digital asset services. FSCA (South Africa) for FX and remittance. AMF/DASP (France) for digital asset services. NCR and SARB (South Africa) for credit and treasury services. Institutional counterparties need a compliant partner. OVEX is that partner.

The Infrastructure Gap Is Closing — From the Bottom Up

The global banks built African FX infrastructure in their image and for their purposes. When Africa stopped being profitable enough, they left. The gap they created is now being filled by institutions that were built for the continent from the start.

This is not a temporary arrangement. It is a permanent shift in how African cross-border finance works. The institutions that move first — the banks, fintechs, corporates, and payment platforms that build relationships with Africa-native FX infrastructure now — will have a structural cost and speed advantage over those that wait.

The old model costs 8–12% and takes a week. The direct route settles today.

OVEX wholesale FX solutions are intended for institutional and professional clients only, and are not available to retail customers. This post is a marketing communication for information purposes only. It does not constitute investment advice, an offer or solicitation to the public. Availability of OVEX products and services is subject to client eligibility, jurisdiction and the applicable OVEX group entity, and is limited to activities permitted under the licences and registrations held by those entities.

Full terms and regulatory information are available at www.ovex.com